Tweet

Tweet

Re: Claim discontinued, Cabot now claiming.

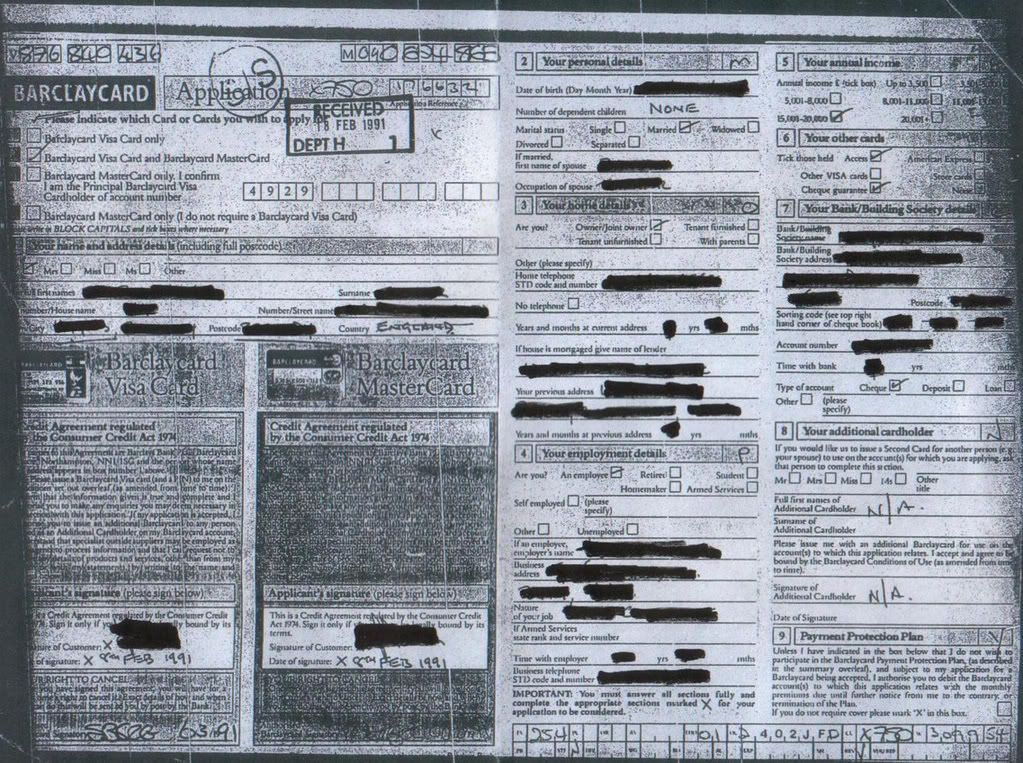

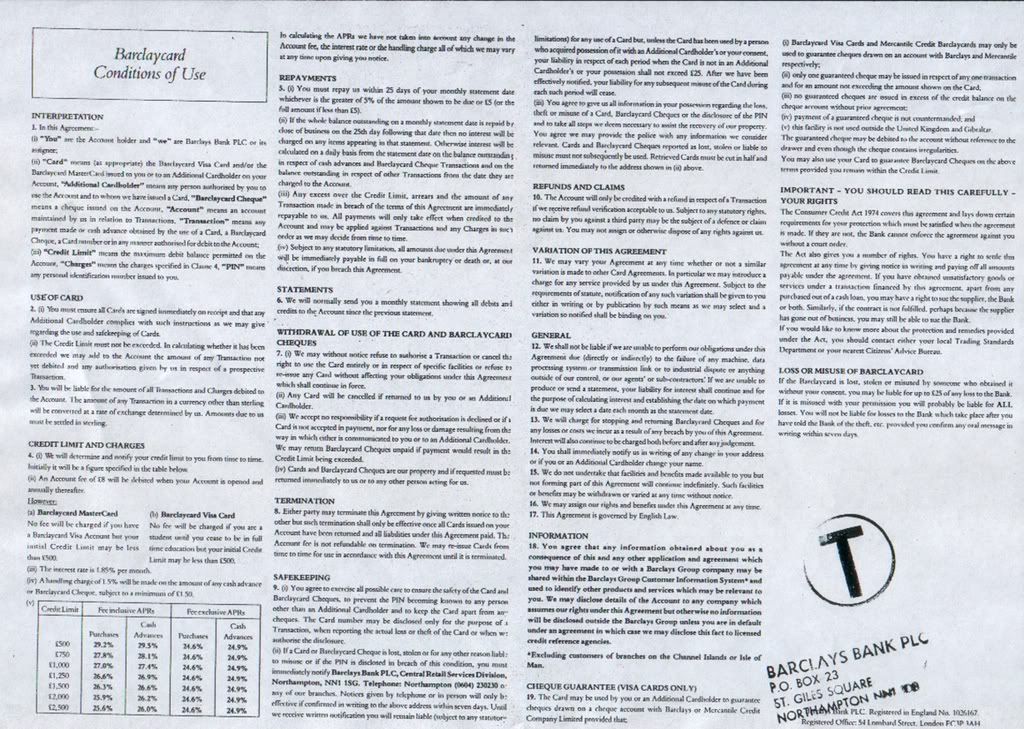

By the way, I really do need to get in some sort of defence to Northampton in the next few days. How do I defend this..............please.

V

By the way, I really do need to get in some sort of defence to Northampton in the next few days. How do I defend this..............please.

V

Comment