Tweet

Tweet

Hi,

we have another thread under the welcome forum http://legalbeagles.info/forums/show...otice-Question but claim has now been received so new thread to keep it fresh.

Issue Date: 10th January 2017

Amount approx: Ł1900

Claimant: Capquest

Solicitor: Restons

Original Creditor: Shop Direct Financial Services Ltd

Particulars of Claim: Please type out in full excluding names/account numbers

The Claimant claims payment of the overdue balance due from the Defendant(s) under a contract between the Defendant(s) and Shop Direct dated on or about Aug xx 2007 and assigned to the claimant on Dec 21 2012

PARTICULARS a/c no - xxxxxxxx

DATE 09/11/2016

ITEM Default Balance

VALUE xxxx.xx

Post Refrl Cr NIL

TOTAL xxxx.xx

Is the debt Statute Barred? No

List any letters you have sent:

Sending CPR Monday 16th Jan

Any other info.

The "contract" was with Marshall Ward and then in about 2009 changed to ISME, the account never became Very.

Sent CCA request to Capquest back in 2013, didn't fully comply with the request so sent a second letter advising them of the error and asking them to rectify, to date no response (we didn't send the second letter by recorded post, which in hindsight we should have done).

When Restons got involved late 2016, we sent a CPR request believing their letter to be a LBA they reponded with the standard "you have not signed it letter so we wont send anything", so we wrote back signing the letter this time, they then wrote back saying if payment was not made within 14 days they would issue a claim, the letter also said that they are not aware of any CCA request being made (the one from 2013 doesn't count?), and that we would have copies of the DN, Assignment, statements etc so they do not need to provide them.

Sent SAR to Shop Direct both in 2013 and 2016.

Copies of letters, DN etc will be posted shortly.

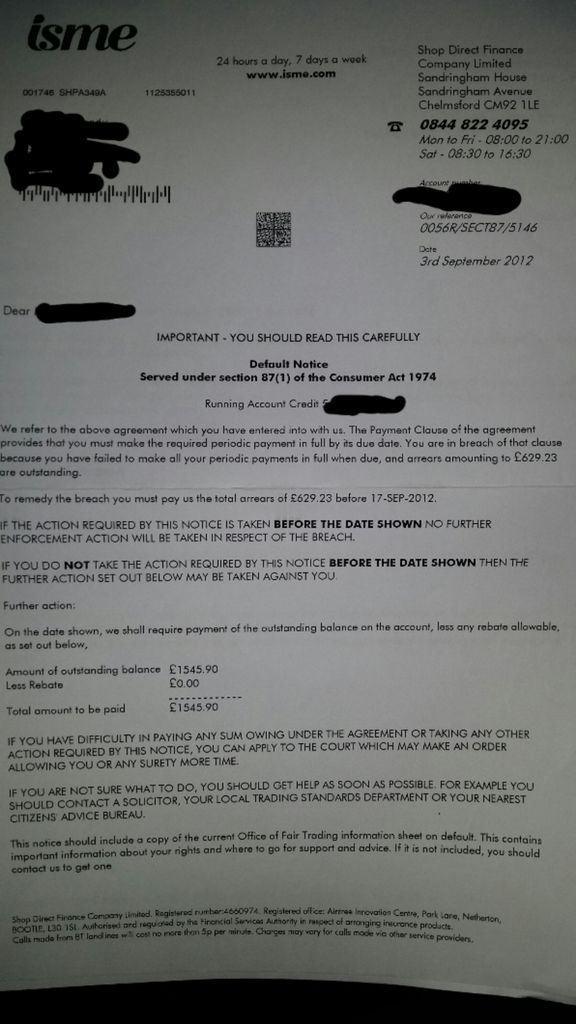

1: The DN we know is bad in that it doesn't allow the 14 days to rectify maybe other bits too but need to check up.

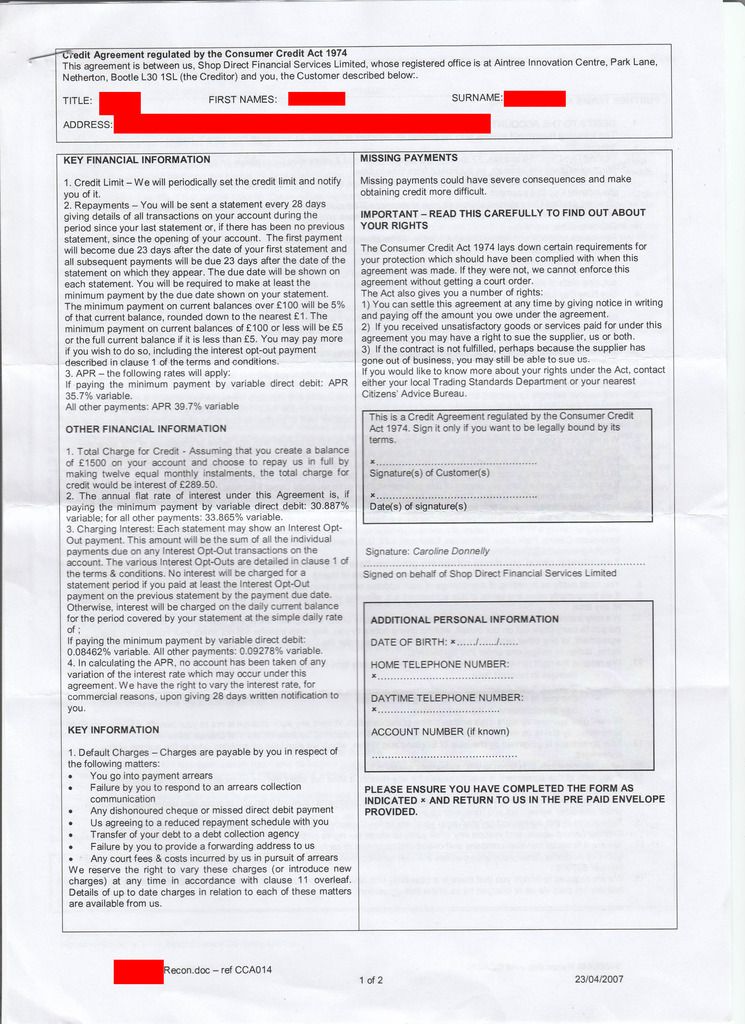

2: The Agreements and T&C's sent by Capquest back in 2013 in response to the CCA request, the first one "might" be ok but the second one (supposedly from when account was closed) is definitely wrong, on wayback it has snapshots of the Terms and they are totally different from the ones sent.

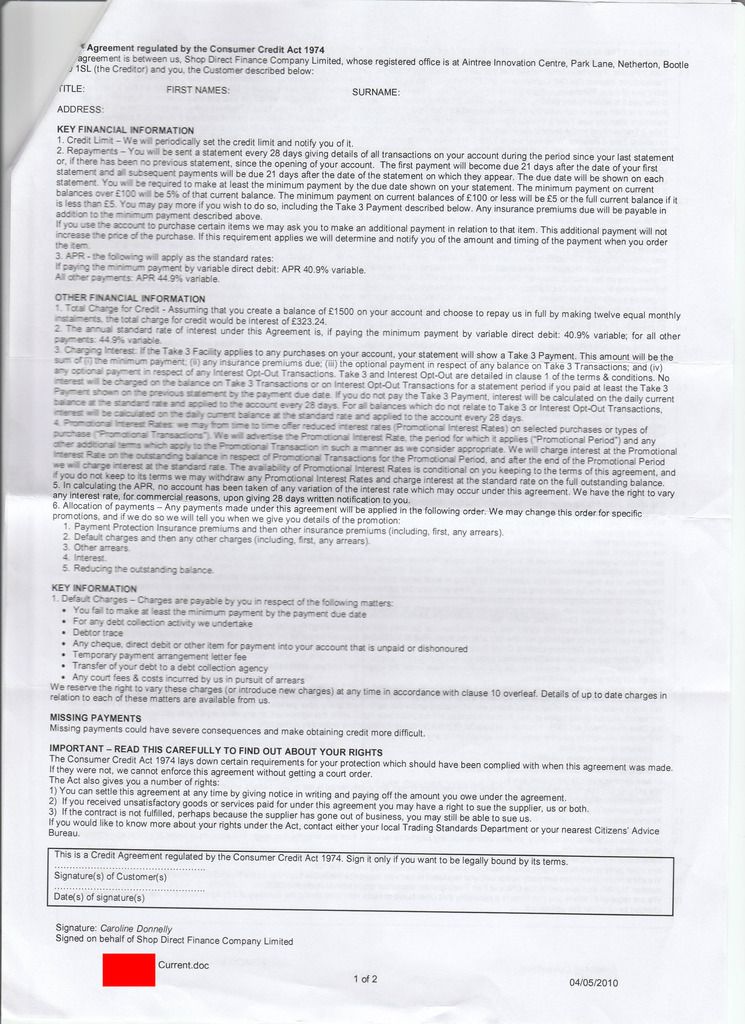

3: In the SAR from Shop Direct the statements state interest charge with the code 197K, on the printout supposed to make it easier to understand their codes it states in bold capitals 197K LX DIRECT ONLY after digging around LX Direct was Littlewoods Extra and Littlewoods Direct, which had it's own website LX Direct, checking the agreements for this part of Shop Direct shows the agreement is made between Littlewoods Financial Services Ltd and NOT Shop Direct Financial Services Ltd.

Now, we intend to try and defend the claim, we don't mind paying the arrears on the original default notice if need be, however, after getting the paperwork back from Shop Direct we had already paid back more than we had bought and if they had been a bit more responsive to the financial situation at the time (Littlewoods stopped charges and accepted reduced payments to get us back on track) ISME refused then we would not have got into this mess!!

On the POC they say the contract was with Shop Direct.

It was with Shop Direct Financial Services Ltd will this make a difference?

The DN, doesn't have the 14 days to remedy they forgot to allow for postage, and includes a host of late, missed, default charges.

Failure to respond properly to CCA request in 2013, should prevent CCJ until fully complied with, is this still the case, or do I really need to send off another request (dont want to give them the opportunity to rectify now if I can help it) besides Restons say we will have copies of agreements....?

The T&C's at the time of termination / default are wrong, will this make any difference?

The correct ones from ISME in 2012 state the order of payment application and default charges etc.

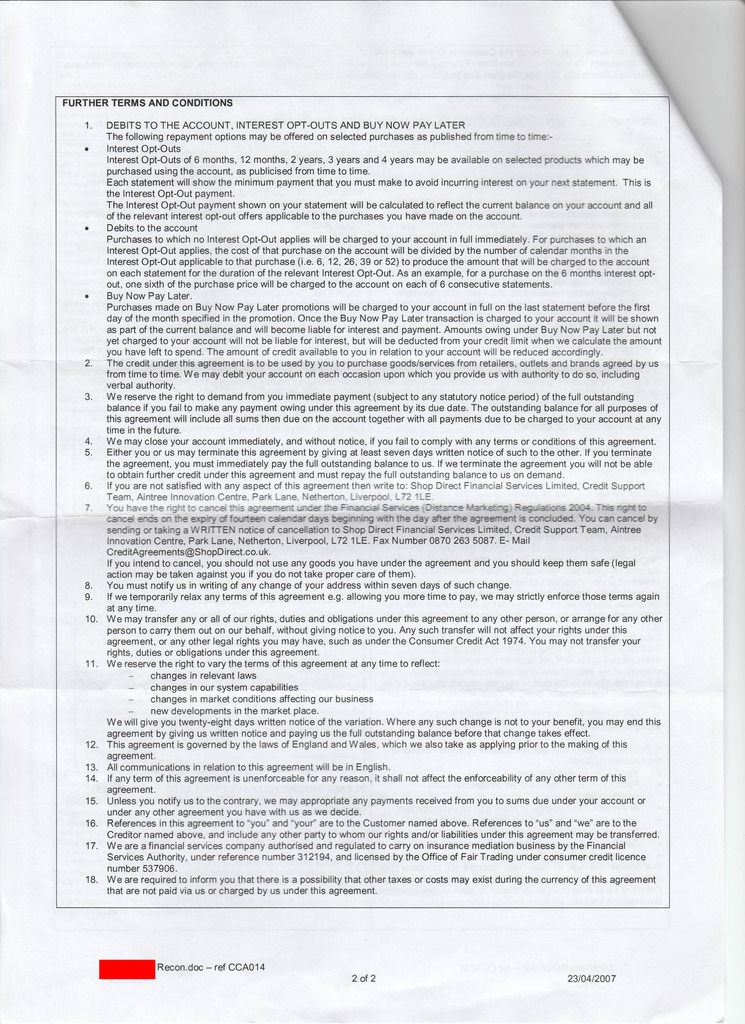

In the T&C's it states under "Key Information" Details of upto date charges in relation to each of these matters are available from us.

Should these have been included as part of the CCA request as other things mentioned within the agreement?

The 197K interest code from LX DIRECT, is incorrectly applied to the account as the account never was anything to do with Littlewoods or LX Direct although I understand Shop Direct own all the brands, the agreement was with Shop Direct Financial and NOT Littlewoods Financial. The interest rate with LX Direct is also lower than Marshall Ward and ISME.

Another thing that is probably very trivial, but the assumed balance they state is Ł1500 on both agreements, however, from reading bits and pieces the assumed balance should be Ł1200? source: The Consumer Credit (Total Charge for Credit) Regulations 2010 (Regulation 6 o)

The claim is also in the Maiden name, been married since late 07, but pretty sure we let Shop Direct know would have been early 08, but there is a chance we forgot them, however in letters to shop direct we signed them with the married name.

From the info I have mentioned in your opinion is it worth trying to defend? or is any defence based on the info likely to get blown out?

In the CPR request, I know I can only ask for documents mentioned, so that is the Contract and Assignment, however they also mention a default balance so can I ask for the DN as technically there can't be a default balance without a DN can there?

Many thanks and thank you in advance.

we have another thread under the welcome forum http://legalbeagles.info/forums/show...otice-Question but claim has now been received so new thread to keep it fresh.

Issue Date: 10th January 2017

Amount approx: Ł1900

Claimant: Capquest

Solicitor: Restons

Original Creditor: Shop Direct Financial Services Ltd

Particulars of Claim: Please type out in full excluding names/account numbers

The Claimant claims payment of the overdue balance due from the Defendant(s) under a contract between the Defendant(s) and Shop Direct dated on or about Aug xx 2007 and assigned to the claimant on Dec 21 2012

PARTICULARS a/c no - xxxxxxxx

DATE 09/11/2016

ITEM Default Balance

VALUE xxxx.xx

Post Refrl Cr NIL

TOTAL xxxx.xx

Is the debt Statute Barred? No

List any letters you have sent:

Sending CPR Monday 16th Jan

Any other info.

The "contract" was with Marshall Ward and then in about 2009 changed to ISME, the account never became Very.

Sent CCA request to Capquest back in 2013, didn't fully comply with the request so sent a second letter advising them of the error and asking them to rectify, to date no response (we didn't send the second letter by recorded post, which in hindsight we should have done).

When Restons got involved late 2016, we sent a CPR request believing their letter to be a LBA they reponded with the standard "you have not signed it letter so we wont send anything", so we wrote back signing the letter this time, they then wrote back saying if payment was not made within 14 days they would issue a claim, the letter also said that they are not aware of any CCA request being made (the one from 2013 doesn't count?), and that we would have copies of the DN, Assignment, statements etc so they do not need to provide them.

Sent SAR to Shop Direct both in 2013 and 2016.

Copies of letters, DN etc will be posted shortly.

1: The DN we know is bad in that it doesn't allow the 14 days to rectify maybe other bits too but need to check up.

2: The Agreements and T&C's sent by Capquest back in 2013 in response to the CCA request, the first one "might" be ok but the second one (supposedly from when account was closed) is definitely wrong, on wayback it has snapshots of the Terms and they are totally different from the ones sent.

3: In the SAR from Shop Direct the statements state interest charge with the code 197K, on the printout supposed to make it easier to understand their codes it states in bold capitals 197K LX DIRECT ONLY after digging around LX Direct was Littlewoods Extra and Littlewoods Direct, which had it's own website LX Direct, checking the agreements for this part of Shop Direct shows the agreement is made between Littlewoods Financial Services Ltd and NOT Shop Direct Financial Services Ltd.

Now, we intend to try and defend the claim, we don't mind paying the arrears on the original default notice if need be, however, after getting the paperwork back from Shop Direct we had already paid back more than we had bought and if they had been a bit more responsive to the financial situation at the time (Littlewoods stopped charges and accepted reduced payments to get us back on track) ISME refused then we would not have got into this mess!!

On the POC they say the contract was with Shop Direct.

It was with Shop Direct Financial Services Ltd will this make a difference?

The DN, doesn't have the 14 days to remedy they forgot to allow for postage, and includes a host of late, missed, default charges.

Failure to respond properly to CCA request in 2013, should prevent CCJ until fully complied with, is this still the case, or do I really need to send off another request (dont want to give them the opportunity to rectify now if I can help it) besides Restons say we will have copies of agreements....?

The T&C's at the time of termination / default are wrong, will this make any difference?

The correct ones from ISME in 2012 state the order of payment application and default charges etc.

In the T&C's it states under "Key Information" Details of upto date charges in relation to each of these matters are available from us.

Should these have been included as part of the CCA request as other things mentioned within the agreement?

The 197K interest code from LX DIRECT, is incorrectly applied to the account as the account never was anything to do with Littlewoods or LX Direct although I understand Shop Direct own all the brands, the agreement was with Shop Direct Financial and NOT Littlewoods Financial. The interest rate with LX Direct is also lower than Marshall Ward and ISME.

Another thing that is probably very trivial, but the assumed balance they state is Ł1500 on both agreements, however, from reading bits and pieces the assumed balance should be Ł1200? source: The Consumer Credit (Total Charge for Credit) Regulations 2010 (Regulation 6 o)

The claim is also in the Maiden name, been married since late 07, but pretty sure we let Shop Direct know would have been early 08, but there is a chance we forgot them, however in letters to shop direct we signed them with the married name.

From the info I have mentioned in your opinion is it worth trying to defend? or is any defence based on the info likely to get blown out?

In the CPR request, I know I can only ask for documents mentioned, so that is the Contract and Assignment, however they also mention a default balance so can I ask for the DN as technically there can't be a default balance without a DN can there?

Many thanks and thank you in advance.

Comment