Tweet

Tweet

EVER since the money markets capsized last August, top bankers have criticised Britain's central bank for a tardy and inadequate response to the gravest financial shock since the early 1930s. Now they no longer have cause to grumble. The Bank of England has taken a decisive step to restore confidence in the banking system.

The “special liquidity scheme” launched this week puts Britain's central bank at the forefront of international attempts to arrest the financial crisis. Although some have called the plan, which is likely to provide banks with at least Ł50 billion ($100 billion) of extra liquidity, a “bail-out”, Mervyn King, the Bank of England's governor, rejects that charge. He said on April 21st that the scheme was “designed to improve the liquidity position of the banking system and raise confidence in financial markets while ensuring that the risk of losses on the loans they have made remains with the banks”.

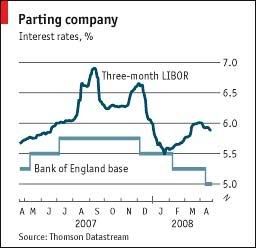

The initiative is a modern version of the time-honoured centralbanking practice of ensuring that solvent banks do not trip up in troubled times for want of ready cash. The need for the Bank of England to reinterpret this sacred text has been apparent for several weeks. A telltale sign of the continuing distrust in and among banks has been the elevated interest rate at which they lend to one another for three months. This LIBOR rate, off which much lending is priced, is normally close to the central bank's base rate. The gap widened extraordinarily when the financial shock started last August (see chart). After falling back at the start of this year, the spread has recently opened up again.

The “special liquidity scheme” is similar to the $200 billion “term securities lending facility” which the Federal Reserve announced on March 11th. Like the American scheme, it involves the central bank swapping easily tradable assets for illiquid assets that the banks are holding. The British facility will let banks swap mortgage-backed and other securities for bills issued by the Treasury.

But three features of the British scheme make it more ambitious than its American counterpart. The first is that there is no cap on its size; and the expected initial take-up of Ł50 billion will be bigger, given the relative size of the two economies, than America's facility. Second, the asset swaps will not be provided through weekly auctions, as in America, but will be available to banks on demand at any time over the next six months. The third difference is that the swaps will be much longer than the Fed's, which extend for just 28 days. Instead they will last for a year and indeed, after renewal, for as long as three years.

Taxpayers are at risk, but there are several safeguards to protect them. Only high-quality securities will be accepted, and a fee will be charged. Banks will get less back in Treasury bills than the value of the assets they are swapping. For example, a bank offering mortgage-backed securities would receive roughly between 70% and 90% of their worth in Treasury bills; and it would have to provide more assets or return some of the bills if the value of the securities then fell. Taxpayers will have to pay up only if a bank defaults and the central bank has incurred losses on its swaps.

Although no explicit deal has been struck, the banks will clearly have to play a part now in resolving the financial crisis. But their side of the bargain will not entail steps to ease conditions in the mortgage market, as Alistair Darling, the chancellor of the exchequer, has suggested. The Bank of England has deliberately limited the assets eligible for the swaps to those existing at the end of 2007, which means that the facility cannot be used to finance new lending. Banks and building societies have been toughening the terms on which they extend new home loans and refinance old ones because they are recognising risk that they had underestimated before.

The Bank of England's scheme is designed to underpin the banking system, not to prop up the housing market. The quid pro quo expected of bankers is that they strengthen their balance-sheets. They must write down losses realistically and boost their capital. Painful though this will be, it is an essential part of rebuilding the financial system.

The “special liquidity scheme” launched this week puts Britain's central bank at the forefront of international attempts to arrest the financial crisis. Although some have called the plan, which is likely to provide banks with at least Ł50 billion ($100 billion) of extra liquidity, a “bail-out”, Mervyn King, the Bank of England's governor, rejects that charge. He said on April 21st that the scheme was “designed to improve the liquidity position of the banking system and raise confidence in financial markets while ensuring that the risk of losses on the loans they have made remains with the banks”.

The initiative is a modern version of the time-honoured centralbanking practice of ensuring that solvent banks do not trip up in troubled times for want of ready cash. The need for the Bank of England to reinterpret this sacred text has been apparent for several weeks. A telltale sign of the continuing distrust in and among banks has been the elevated interest rate at which they lend to one another for three months. This LIBOR rate, off which much lending is priced, is normally close to the central bank's base rate. The gap widened extraordinarily when the financial shock started last August (see chart). After falling back at the start of this year, the spread has recently opened up again.

The “special liquidity scheme” is similar to the $200 billion “term securities lending facility” which the Federal Reserve announced on March 11th. Like the American scheme, it involves the central bank swapping easily tradable assets for illiquid assets that the banks are holding. The British facility will let banks swap mortgage-backed and other securities for bills issued by the Treasury.

But three features of the British scheme make it more ambitious than its American counterpart. The first is that there is no cap on its size; and the expected initial take-up of Ł50 billion will be bigger, given the relative size of the two economies, than America's facility. Second, the asset swaps will not be provided through weekly auctions, as in America, but will be available to banks on demand at any time over the next six months. The third difference is that the swaps will be much longer than the Fed's, which extend for just 28 days. Instead they will last for a year and indeed, after renewal, for as long as three years.

Taxpayers are at risk, but there are several safeguards to protect them. Only high-quality securities will be accepted, and a fee will be charged. Banks will get less back in Treasury bills than the value of the assets they are swapping. For example, a bank offering mortgage-backed securities would receive roughly between 70% and 90% of their worth in Treasury bills; and it would have to provide more assets or return some of the bills if the value of the securities then fell. Taxpayers will have to pay up only if a bank defaults and the central bank has incurred losses on its swaps.

Although no explicit deal has been struck, the banks will clearly have to play a part now in resolving the financial crisis. But their side of the bargain will not entail steps to ease conditions in the mortgage market, as Alistair Darling, the chancellor of the exchequer, has suggested. The Bank of England has deliberately limited the assets eligible for the swaps to those existing at the end of 2007, which means that the facility cannot be used to finance new lending. Banks and building societies have been toughening the terms on which they extend new home loans and refinance old ones because they are recognising risk that they had underestimated before.

The Bank of England's scheme is designed to underpin the banking system, not to prop up the housing market. The quid pro quo expected of bankers is that they strengthen their balance-sheets. They must write down losses realistically and boost their capital. Painful though this will be, it is an essential part of rebuilding the financial system.