Tweet

Tweet

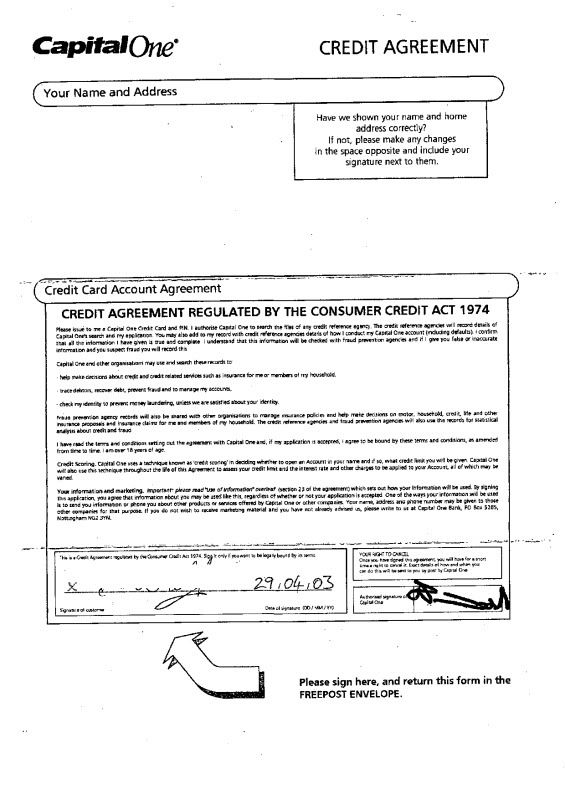

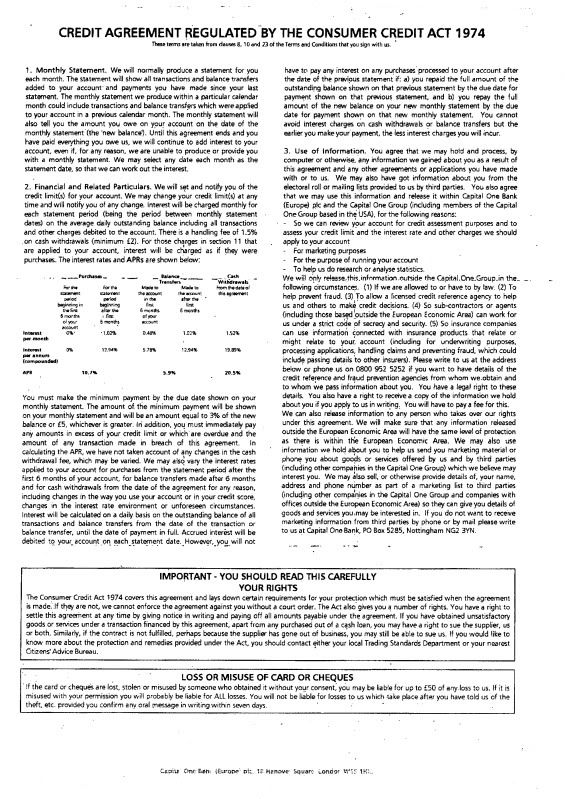

I have been playing letter tennis with Cap1 for sometime now, and finally, many months after the initial request, have been provided with a copy of what they are saying is a fully enforceable agreement. As I understand, one of the prescribed terms for a credit card agreement is a credit limit - sadly lacking on what has been provided to me.

I've read so many sites and forums about this issue that I'm now more than a little confused. So, what I'll put here is what I would like to do, if it's possible....

I believe that I've read somewhere that if the agreement was not drawn up correctly, then Cap1 didn't really have the right to charge me interest and charges (isn't there a case where the Judge ruled that without a properly executed agreement, all monies could be classed as a 'gift'? - I'd like to be able to refer to that in the letter I am currently trying to write).

So, what I intend to do at this moment, is write back to Cap1, pointing out to them that prescribed terms are missing, and therefore the agreement is unenforceable and probably invalid. Calculate how much interest I have paid according to the information they have provided me with, deduct this amount from the balance, and get them (somehow) to agree to accepting a final payment of the reduced balance. Technically, I guess I'm not actually claiming back charges, just requesting they be offset against the balance. I know it's a long shot, but .....

There are only about Ł40 #(2 x Ł20) in penalty charges throughout the term of the card, and no PPI charges at all.

It's possible (they do seem to make many mistakes) that they will write back pointing out something along the lines of the lack of prescribed terms doesn't give me the right to claim back interest, just that the agreement is unenforceable - I can dream can't I?

I have previously had advice from another web-site, but all the experts seem to have disappeared which of course, led me to google for information and lo and behold, I found myself here.

which of course, led me to google for information and lo and behold, I found myself here.

Please be gentle with my, my brain doesn't work as well as it should, and sometimes I need things explaining to me in very simple terms.

Looking forward to receiving responses though.

I've read so many sites and forums about this issue that I'm now more than a little confused. So, what I'll put here is what I would like to do, if it's possible....

I believe that I've read somewhere that if the agreement was not drawn up correctly, then Cap1 didn't really have the right to charge me interest and charges (isn't there a case where the Judge ruled that without a properly executed agreement, all monies could be classed as a 'gift'? - I'd like to be able to refer to that in the letter I am currently trying to write).

So, what I intend to do at this moment, is write back to Cap1, pointing out to them that prescribed terms are missing, and therefore the agreement is unenforceable and probably invalid. Calculate how much interest I have paid according to the information they have provided me with, deduct this amount from the balance, and get them (somehow) to agree to accepting a final payment of the reduced balance. Technically, I guess I'm not actually claiming back charges, just requesting they be offset against the balance. I know it's a long shot, but .....

There are only about Ł40 #(2 x Ł20) in penalty charges throughout the term of the card, and no PPI charges at all.

It's possible (they do seem to make many mistakes) that they will write back pointing out something along the lines of the lack of prescribed terms doesn't give me the right to claim back interest, just that the agreement is unenforceable - I can dream can't I?

I have previously had advice from another web-site, but all the experts seem to have disappeared

which of course, led me to google for information and lo and behold, I found myself here. Please be gentle with my, my brain doesn't work as well as it should, and sometimes I need things explaining to me in very simple terms.

Looking forward to receiving responses though.

Comment