Re: Swift Advances Plc?

The ICO have replied to this letter copied below informing me that they are escalating my complaint to their investigations dept

To

The Information Commissioners Office

First Contact Department

For The Attention of XXXX XXXXXXXXX.

Dear XXXXX XXXXXXXXXX

Ref Case Number RFA0385393 Further complain about Swift Advances plc.

Thank you for your letter of 4th July 2011 date, I fully appreciate the workload and

understaffing of the ICO.

I can confirm that I have now received some of the data and information from Swift Advances plc under my second SDAR, however once again they have failed to fully comply with said request.

I have stated on many occasions that Swift Advances plc continually mislead official bodies and even make false statements under oath to the Courts.

I will now proceed to prove that they have misled the ICO, during my previous complaint of 2009 I made the ICO aware of the fact that Swift Advances plc had transferred and assigned our loan to Kestrel Loans No 1 Ltd ( Kestrel No1), and I asked the ICO to force that company to supply the data it was processing about our loan, personal and financial details.

I made the ICO aware of the fact that this company did not hold a data controllers licence to lawfully process data, I also supplied the ICO with all the relevant documents to prove said allegations, I also made the ICO aware of the fact that it held neither a CCA licence issued by the OFT enabling Kestrel No 1, to conduct consumer credit business, and did not hold a licence issued by the FSA.

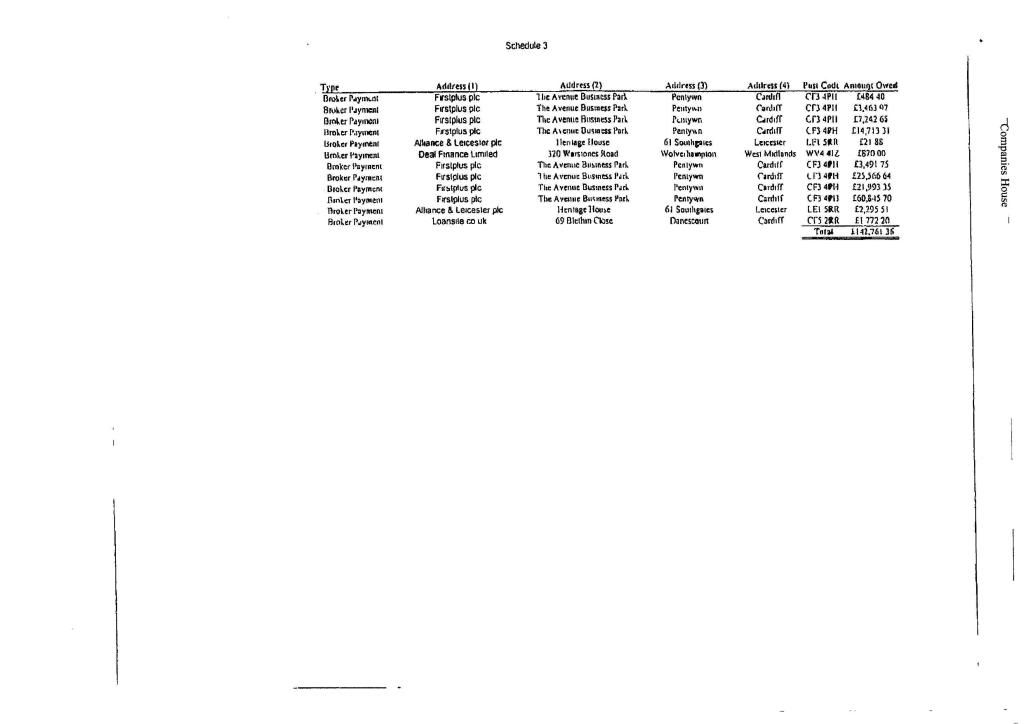

Swift Advances plc falsely told the ICO that the Kestrel Companies ( there are 3 of them) none of which hold said licences, that they are holding companies and do not process data. Holding Companies do not have such a large amount of employees and pay such wages and salaries as shown below in Kestrel Loans No 1 accounts.

The ICO accepted that statement, despite my warnings, that, if they can make false statements under oath they will and did make them to the ICO.

Attached as Exhibit 1, is the statement made by Mr John Webster the Chief Executive of Swift Advances plc staing that loans were transferred to Kestrel No 1.

Here I included the exact copy of their accounts but its in Adobe and did not copy on to this post, but the ICO have this further proof ......had my reply within 5 days ....now that,s quick for the ICO looks like they are moving pretty quick on this letter

I copy extracts from the First set of accounts filed by Kestrel Loans No 1 Ltd

Extracts from Kestrel Loans No 1 First set of audited accounts by KPMG

Principal activities and business review

The principal activity of the company is the provision of finance to individuals, secured on domestic, semi commercial or assured short-hold, freehold and long leasehold properties.

Regulation

The market in which the company operates has bee subject to recent changes in regulation of the Consumer Credit Act 1974.These came into effect on 31st May 2005 and affected the form and content of all new loan agreements entered into by the company which are regulated by the 1974 Act.

The Consumer Credit Bill will also bring about other changes in the credit laws and this is in the early stages of making its way through Parliament. The provisions of the bill are not expected to take effect until Autumn 2007 at the earliest.

Fees and commissions paid Ł666,389

Debtors

Loans Ł102,573,709

Kestrel Loans No 1 Ltd do process data and they are processing it without notification, yet the ICO allows this processing to continue unabated.

Kestrel Loans No1 Ltd is not a holding company as the ICO have been misled to believe by Swift Advances plc. Their yearly accounts submitted to Companies House are absolute prima fascia proof of that they are a fully active company.

I again attach copies of said accounts stating what the Kestrel Companies do,holding companies do not conduct business as shown in Exhibit 2

They are processing data about 1000’s of their customers accounts and loans as stated in those accounts, these loans are secured on borrowers property, again their accounts confirm this, it is called giving misleading information I call it deliberate lies.

All these loans were sold by equitable assignment as is seen in Exhibit 1

I now attach a copy of the underwriting sheet appertaining to our loan, the ICO informed Swift Advances plc that they should supply said underwriting sheet which was supposedly to have had only the so called “commercially sensitive information” redacted. Exhibit 3, you will see that 95% or so of information has been redacted (blocked out), that is a lot of commercially sensitive information would you not agree?

You will note the difference between another “Swift” underwriting sheet which I attach also. Exhibit 4 which shows the full information of what an underwriting sheet is and contains, note the reference to commission, two lots loan commission and PPI commission.

I submit the reason that all the information that has been blocked out (“redacted”) is that it will lend more evidence to the fact that secret commission was paid on our loan that was denied being paid under oath by their witness Mr Mark White, “Swifts” senior manager of their risk assessment department.

You will also note that all information about our First mortgage has been blocked out, plus lots of other information that cannot be classed as sensitive information otherwise it would have been redacted on document. Exhibit 4

It is actions such as these that has led the OFT to impose severe restrictions on Swift Advances plc in relation to their CCA licence.

I asked for a complete history of our account in order to see if any information had been added or deleted from the History notes we received in our first DPA SDAR information,

I also asked for the key code to the codes applicable to said history notes, and have been told by Swift Advances plc there is no requirement for them to supply such key to said codes, and they will not be supplying it.

I also asked for the continued record of payments that are being accounted for on the Kestrel computer system ( the ICO has a copy of the first years payments 2007 to 2008, I asked for the following years, these have been refused to be supplied. The ICO has made it clear that this key must be supplied but again Swift Advances plc flout the DPA and the ICO.

We have been supplied with only some of the information that was passed on to Olympian Finance Ltd, even after the ICO had informed Swift Advances plc they had to supply all of it, our History notes states that other information was supplied but that does not contain the full details of what was supplied.

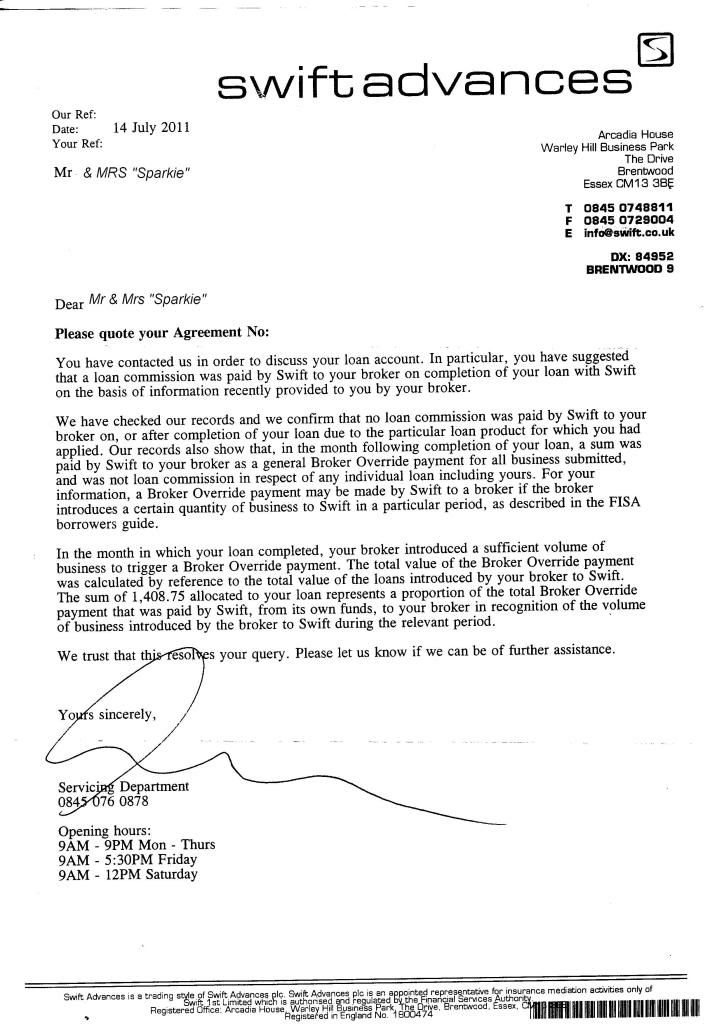

I attach a copy of the letter received from the Managing Director of Promise Solutions Ltd Exhibit 5 confirming that a commission of Ł1408.65 was paid to our broker, that again Mr Webster their CEO stated that no commission was paid on our loan again showing how the senior management continue to make false misleading statements.

The record of said payment will be contained in our underwriting sheet that “Swift” have deliberately blocked out, disclosure of such secret commission would render our agreement void and “Swift” would be forced to return all monies paid by us, for reason further steps have been taken to cover up the payment of said commission, and that is further concealment and deception in anyone’s language.That in itself is also a breach of

the Second Principal of the DPA.

I would accept the word of a convicted thief over the word of these white collar

professional people any day.

This time I hope the ICO will take firm action against this company and the Kestrel Loans companies, as they are not holding companies, and they do process data, there are only two holding companies Kestrel Acquisitions Ltd, and Kestrel Holdings Ltd.

All is needed is a check with Companies House to confirm all I say is correct and all “Swift” have said is false.

Exhibit 6 is a record of our account with Kestrel Loans No 1 and proof that it is that company that is also processing data about us

Yours sincerely

The last time the ICO investigated "Swift" & "Kestrel" companies and I told the ICO they had no CCA licence, FSA licence or DPA licence Swift lied to them and said that the Kestrel Companies were holding companies.......and they just had their wrists smacked ....................now the ICO kbow that they have been lied to.

I do not think they just have their wrists smacked this time.

Loading...

-

Re: Swift Advances Plc?

Friend of mine has just sent me this...........re Section 155 of the CCA...........this covers unregulated agreements. But not FSA agreements

http://www.oft.gov.uk/shared_oft/rep...dit/oft301.pdf

SparkieLeave a comment:

-

Re: Swift Advances Plc?

This is what Mark White said in one Court....

But he is being -- sorry. A. (Mark White) Sorry. Swift don’t run a packaging department. We don’t have clerks who write to the Abbey National, to GE, to customers’ employers, to instruct valuations, or any of that type of nature. ( I have copies of letters obtained from Abbey National written to them by "Swift Advances " before we signed our agreement ...again he didn't tell the truth.) What they expect is that a broker will send in a fully packaged set of papers -- I mean, effectively the whole of the first part of this bundle -- with the authorities and declarations, credit agreement, legal charge, valuation, details of the prior mortgages, details of any arrears, Equifax searches. ( Swift also presented a copy of our credit file in court obtained by them from Equifax as well as the one from Promise....they double check a credit file and copy it..another false statement)..........The whole bundle is presented to us as one piece. If the loan goes ahead, we pay a commission which effectively remunerates the broker for us not having to do any of that work at all.

Isn't that what the brokers fees paid for by the borrower are for in our case ....Ł 3325.00 also

Mark White in our case swore on oath that Swift do not pay commission at ALL ...full stop ......blanket statement………Two witness in Court heard him say so from the stand.

SparkieLast edited by Sparkie1723; 15th July 2011, 22:22:PM.Leave a comment:

-

Re: Swift Advances Plc?

I'll be posting in a minute the list of lenders and the brokers fees that Promise Finance Ltd were owed from lenders between May 2006 and April 2009 you will see No Swift company is in there ...this is from the administrators accounts, in his report the administrator says that the commissions they were due to receive would match match the brokers fee roughly 50/50 ie doubled.

Can't see Swift there can you??

Solutions must have been our broker .....and they did not hold a CCA licence

Sparkie

Last edited by Sparkie1723; 15th July 2011, 21:09:PM.

Last edited by Sparkie1723; 15th July 2011, 21:09:PM.Leave a comment:

-

Re: Swift Advances Plc?

Hi All,

Sparkie you definitely seem to be on the right track.....Keep the pressure up and Swift might just crack!

See here.....FSA issues warning on override commissions | News | Mortgage Strategy

AtlantisLeave a comment:

-

Re: Swift Advances Plc?

This is what I will be basing my reply to their letter on

I Did not say when it was paid …….just the fact it that it was, which has finally just been admitted it was.

Checking your records is not accepted …you must provide those records i.e the exact original unredacted underwriting sheet which is where said commission is recorded, which will show no tampering with copies as has been seen to have been done before.

It is irrelevant what you call this payment, the fact of the matter is it was paid and it was undisclosed in the antecedent negotiations and continually denied by Swift even under oath, it was/is a bribe.

This was also denied by Promise Solutions Ltd at first, ( the first time in a phone conversation in 2009 and again in the first contact phone call of this year, until pressure was put on them to tell the truth and reveal this payment, you say it is an "override payment"....... "Promise" refer to it as "override commission".

You must provide evidence to the contrary to our assertion that our loan was the only loan agreed to with “Promise” in the month of April 2007, and all the evidence to show how the total loans for that month warranted the payment of Ł46,955.00 in “override payment” from which this Ł1408.75 was apportioned

You will be required to explain how this payment of Ł 1408 .75 is exactly 3% of the total value of our loan amount which was Ł46,955.00.

It will be hard to expect the court to consider that this is merely a coincidence, how ever I am sure you will put forward some kind of unacceptable explanation.

Why don’t you tell me the truth for once??

:violin:Last edited by Sparkie1723; 15th July 2011, 19:59:PM.Leave a comment:

-

Re: Swift Advances Plc?

It's obvious Swift are panicking. Sparkie was never informed that a payment from Swift of circa Ł1,400 would be oportioned to his loan agreement.

There's a saying: You can't polish a turd but, you can roll it in glitter.Last edited by Ihaterbs; 16th July 2011, 09:06:AM.Leave a comment:

-

Re: Swift Advances Plc?

This is what went on after the HUrstanger rulig that ruled against the lender because it was a claim against the lender.

"Prestige Finance has reviewed its position at length in relation to the findings in the Hurstanger versus Wilson case. After careful consideration of the judgment and discussion with legal advisers, we now have to disclose the amount of commission payable to the broker."

A heated debate is believed to have broken out at a recent Finance Industry Standards Association regarding whether lenders need to disclose the commission.

John Webster, group chief executive at the Swift Group, feels that it is not an issue for lenders to address, but that the emphasis rests on the brokers, as they are the ones that have the first point of contact with the customers. He says: "I don't think it's a disclosure issue for lenders, but for the intermediary instead.

Mr Webster is pointing the finger at brokers in an attempt to escape the truth........looks bad for Mr Walker MD of Promise Solutions Ltd.

"If you look at a normal transaction, the lender discloses the amount of commission and whether they were in receipt of any potential override after the intermediary. It is at the point of sale that this should be disclosed."

Webster says it will be writing to its brokers to clarify what it feels they should disclose.

Sparkie

There is much case law on all this .....this is just some of them

Bristol & West Building Society V Mathews (1998 CH1 Lord Justice Millett

The Broker as agent has a duty Not to make a secret profit. The agent is entitled to receive a fee as remuneration for his service or/and a commission which is the ordinary amount which agents are in the habit of charging. The implications of this is if there is no indication or reference to a payment of commission, there is a strong argument to support the contention that a secret commission has been paid.

Shipway v Broadwood [1899] 1QB 369). According to Lord Chitty:

"The real evil is not the payment of money, but the secrecy attending it."

Attorney General for Hong Kong v Reid [1994] 1 AC 324

"Bribery is an evil practice which threatens the foundations of any civilised society."

. The consequences of receiving/gifting secret commission are serious. " Criminal Justice Act"......used to be covered by the Prevention of Corruption Act 1906

This is the one I will be basing my claim on.....it was never disclosed until the last few days..........................Backed up with all the others.

SparkieLast edited by Sparkie1723; 15th July 2011, 16:46:PM.Leave a comment:

-

Re: Swift Advances Plc?

Had a letter from "Swift Avances" servicing department no name at the bottom of the letter just a squiggle as usual...........I'll post it up later .......this is the first time that they admit that they paid this payment to "our broker"....BUT they do not name the broker ...........they also use the same terminology that the MD of Promise Solutions Ltd did .......an override commission..............and "Swift Advances" are now saying that they paid this out of their own funds ..............they haven't got their own funds never had .....they use borrowed money .......100's of millions of it......even so when our loan was set up "Swift Advances" was an unlicensed trading name that belonged to another company.

Who do they think they are kidding.......must think I came off a bannana boat. No matter where it came from its ...a bribe ....a backhander.........a bung. JUst think of the amount of money they pay and paid "out their own funds" ......they wouldn't have any left to lend.

I now have the evidence that the only loan that "Promise" arranged through any/either of the "Swift" companies in April 2007 was ...................OURS.

There is no record of our loan brokers fee commission in Promise Finances Ltd accounts ( First plus , Blemain G.mac Ge Money, Bank of Ireland, Nationwide etc etc etc ......BUt no "Swift" company.

Therefore our broker was/must have been " Solutions" and ........they did not hold a CCA licence....of course the OFT are being made aware of this

Sparkie

Here is their latest rendition

If you compare the wording of the last paragraph with the wording of the letter from the MD of Promise Solutions ltd on the the new thread I started on Promise Finance Ltd you would swear they were written by the same person.....so who has been talking to who do you think??!!Last edited by Sparkie1723; 15th July 2011, 14:57:PM.Leave a comment:

-

Re: Swift Advances Plc?

Now I have the evidence I can now take action against both "SwifT and Promise" for undisclosed denied Sectret commission.

That's what the law says about this...............an action can be taken against against either the payer or the recipient..............this is the way to get Mr White, Mr Webster and Mr Walker in the same Court room...........that will be very interesting ...........letters before action are being sent to day by e-mail and recorded delivery.

Just a burst across the Bows for starters

There will also be some some sparks flying because Promise Finance Ltd held a CCA licence but did not have an ICO licence Promise Solutions did not have a CCA licence but held an ICO licence....neither were on each others as a trading name!!

a LTD company cannot be a trading name on a licence ......................each one has to hold their own separate licence.

Both the OFT and the ICO are being made aware of the Company Number that was used by Promise Solutions Ltd to buy Promise Finance Ltd from the administrator.........I'll put my reasons for this later and I firmly believe what I will post.

I have also got a full list of the inventory that Promise Solutions Ltd bought which included Dell computer monitors and base units (10) lap tops...servers ....window servers licencing packs hard drives Krahl com servers a further 9 computer base ........these would have held evry single bit of information that Promise Finance Ltd had ........and they try to tell me and ounits ne of their other customers they only have "very limited info"...........I leave you all to make your mind up if that is to believed..........remember the only way data can be deleted from a computer is that the hard drive MUST be physically destroyed.

SparkieLast edited by Sparkie1723; 15th July 2011, 08:50:AM.Leave a comment:

-

Re: Swift Advances Plc?

It may be a good thing that Promise Solutions Ltd will not repay our now admitted undisclosed commission as it opens the door for me to summon Mr White back into Court to explain his statement under oath that they did not pay this commission that Promise Solutions Ltd say they received......( Ł1408.65)

This is better than them paying us our commission back………Mr Whites perjury can void our agreement title charge and Swift Advances plc will have to repay us all our money back costs, compensation in restitution …….I feel quite happy today.

The MD of “Solutions” is now caught up in the whole goings on.

SparkieLeave a comment:

-

Re: Swift Advances Plc?

Police came to see me again today had a good meeting /interview....a detective Sgt from the fraud squad will be contacting me very soon to arrange a time to pay me a vist with a colleague .....the officer studied the two letters I posted in the first post and took copies of them away .

It appears that in view of Mr Whites statement about commissions not being paid under oath will more than likely draw Promise Solutions Ltd into the mixing bowl.

They want to play awkward.....that's their problem now

SparkieLeave a comment:

-

Re: Swift Advances Plc?

You did say youwere playing devils advocate and that is what I appreciate Peter and thank you .......you have to get all angles of an argument and that is the only way.......... get someone to argue against instead of agreeing or putting up another angle.

SparkieLeave a comment:

-

Guest repliedRe: Swift Advances Plc?

Guest repliedRe: Swift Advances Plc?

I think the answer would be that the CCA did not set the financial limit in order to ensure that the loan given was under 25K but to ensure that the amount recoverable under the individual contract did not exceed 25K.

This restriction would be held no matter how many contracts were issued for a single purchase.

It in effect limits the liability of a single contract.

PeterLeave a comment:

-

Guest repliedRe: Swift Advances Plc?

Did say i was playing devils advocatre here by the way.Originally posted by Sparkie1723 View Post

The thing is the act says that a creditor cannot lend a debtor more than 25K, doesnt say in a single agreement. I am sure that they would say that all they were doing wa following the act.

If this was allowed then what would be the point of having a financial limit at all?

I am sure it is not a breach of statute but would not presenting the option be considered unfair?

Peter

PeterLeave a comment:

Leave a comment: