Re: Swift Advances Plc?

Hello i am new here and desperately needing some help dont know who to trust anymore, swift are trying to take our home which is also an animal sanctua:tinysmile_kiss_t4::beagle:ry, It would appear when i start to ask questions they tell me theres is nothing i can do, they have lost paperwork and door upon door is closed in my face, firstly we were sold this through a guy called matt hodgson from global reach services, (gone) he got valuation allied surveyours, ian frost. he has run away and allied surveyours are now in liquadition but set up again as allied dilengently, the point i am trying to make firstly is ian frost over valued property by more than 50% its true worth, we have proof of this five independant valuations, we have tried to get comp from insurers but allied is now liquadated, the other point i am making is we would never have acted or taken out any loan if we had known true valuation.

Also the paperwork i have has two signtures on and they arent mine, have asked swift for all copies of agreements from them, i am still waiting, weeks now and they have eviction date set for us 19th july, we have no solicitor cant afford one and dont know who to trust anymore, I am appealing via the court system but no one there is bothered and i get the ipression that they all think it is pointless what i am trying to do. I am trying to save our home and more to me than that, the sanctuary, we have only acted upon the influences of others, professional others that are suppose to know what they are doing, how is it then, that through their faults and mistakes we all have to pay the price. I chained myself to the angel of the north a few years ago i protest, i feel now that the only way to be heard it to shout as loud as we can instead of others trying to silence us for good. Our own web site is available for anyone to set up forum on, united as one, all help welcome.

Oh and i have them on tape telling me they have lost documents, then telling me that they are archived. everytime i have been in court they make me feel like nothing, them and their fancy lawyer and me on my own, who is the law for anyway?

Loading...

-

Re: Swift Advances Plc?

Swift shocked by OFT's threat to cancel licence

27 June 2011

Sub-prime lender Swift says it is surprised at the Office of Fair Trading’s threat to remove its consumer credit licence last week after discovering poor lending practices.

Swift, trading as Swift Advances and Swift Securities, is regulated under the Consumer Credit Act for second charge lending and by the Financial Services Authority for first charge mortgages.

Last week the OFT revealed that it has ordered the lender to improve its practices or risk losing its licence. It could also be fined up to Ł50,000.

Its investigation found the lender was failing to check whether applicants could afford the loan or to verify their income. It also did not fully check information in applications.

The OFT also uncovered evidence that in some cases Swift failed to fully explain the charges that could be incurred if customers fell into arrears and failed to exhaust alternative options before taking borrowers to court.

Mortgage Strategy revealed in December 2010 that Swift was being investigated by the FSA for its handling of borrowers in arrears and had set aside Ł9.4m to cover a potential fine and other costs.

But a spokesman for Swift says: “We were surprised by the tone of the OFT press release. At no point during the investigation or during the adjudication procedure was it suggested that Swift’s licence was in jeopardy.”

Rubbish they were warned publicly around November 2010???....Sparkie

But David Fisher, director of consumer credit at the OFT, says: “Credit businesses must lend responsibly and failure to do so can have a serious impact on borrowers. We require Swift to significantly improve the way it carries out its business. If it fails to comply with these requirements, it will face further enforcement action.”

Another Press release

Watchdog raps Alchemy firm Swift

24 Jun 2011

One of the country's largest subprime lenders, owned by the major private-equity firm founded by Jon Moulton, has been rapped over the knuckles by the Office of Fair Trading.Swift, which trades as Swift Advances and Swift Securities, was warned it could have its credit licence revoked if it does not improve its act rapidly.

Swift is owned by Alchemy, the Ł1 billion private-equity group which Moulton quit two years ago after falling out with management.

SparkieLast edited by Sparkie1723; 29th June 2011, 11:09:AM.Leave a comment:

-

Re: Swift Advances Plc?

Hi TINKEY 2,Originally posted by TINKEY2 View Post

Then again you have to remember the last time someone had a dream.........he got assassinated!!!!

SparkieLeave a comment:

-

Re: Swift Advances Plc?

That made me smile, I don`t think they will find A director who will sign it!!

TT:cheer2:Leave a comment:

-

Re: Swift Advances Plc?

On the lighter side of things, I had a dream last night, I dreamt I found this in a dustbin down south somewhere......and for the life of me I can't remember where

An Interim Directors Report

It has been a difficult year for the company, the forecasts of previous reports have come under severe attacks from a certain band of customers who unlike most of our other customers who we could control by our bullying tactics, were not controllable, no matter how we tried to abuse them, this small band and others have caused us a considerable number of problems and extra work and we face financial fines by the authorities.

We are trying to rectify matters by gaining more house possessions in the shortest possible time by using our same old tried and tested techniques of allegedly lying to the courts and misleading the Judges, it has been easy in the past because they do not have the time to check up on what we tell them.

The company is slowly encountering more and more resistance from our customers and it is not possible to predict the long term outcome of the events that are taking place.

Some customers have found out more than what they should have done, such as our double accounting, false accounting, and "irregular borrowing", we are doing our best to cover our tracks on these issues, only time will show if we achieve this, but our select band of shareholders can be assured we are trying to keep up the generous supply of this extra money.

We will continue to lie our way through these trying times and hope we are believed as we have been in the past, rest assured that we do have a contingency escape plan by which all will more likely to be able to hold on to our individual stash of cash that will be difficult to trace.

The increase in applications for possessions of borrowers property will continue for as long as possible, we have one thing on our side that will assist us in that quest, the power of money to be able to enjoy the fact we can employ clever unconscionable solicitors and Barristers to act for us at the cost of the borrowers. It has been easy to get these properties in the past . No longer is this so, it is getting more difficult.

Another issue we must consider, we may be forced to repay a lot of charges we have collected by being a little too greedy, and using our unlicensed trading names to apply them, we will have to find another way to apply these, as this is our bread and butter, we cannot run our companies on our interest rates alone, after paying the interest on the funds we have borrowed would leave us with a profit margin of 6 to 7 percent no business can remain trading on a margin such as this, if we lose our charges income.

The directors are sorry for such a dismal report but we have tell the truth for once, and apologise for having to do so

Signed

A director......................................... when we can find one to sign it

Leave a comment:

-

Re: Swift Advances Plc?

For the benefit of the Swift Advances plc trolls, .......I have made the OFT aware that this Monday they applied for repossession of 9 homes in N.Ireland .....another 9 today and have 4 more listed for tomorrow......22 homes in 3 days.........at this rate they will own all the homes in N.Ireland, but that's what they do ........repossess peoples homes

SparkieLeave a comment:

-

Re: Swift Advances Plc?

I have been reading anther forums threads on Swift Advances plc and it sickens me to read of how people are still suffering from the actions of these people and some are asking if they can do anything about Swift Advances plc even though, they have been forced to settle their loans to get away from their abusive, bullying tactics....I would advise that they use Section 140 of the New Consumer Credit Act amendments 2006.The Unfair Relationship.

Under this section the court can re-open agreements that have ended.

Claims can be submitted under this section , and you can challenge" Anything that the creditor has done before the agreement was entered into ...anything that was done during the agreement was in force.......and anything done after the agreement has ended,

Armed with what the OFT independant adjudicator has concluded and placed the restrictions on Swift Advances plc........the Claimant will stand a much better chance on succeeding on a claim made under this section than ever before.........the adjudicator has given you the bullets ,,,,now fire them in your claim.

I believe that this assement and restrictions will guide and assist the Courts into ruling as to what was fair and what was not.

As Iam banned from posting on a certain forum...........it would be advantageous and helpful if this could be pointed out on that forum, to assist other customers obtain fairness and justice.

Sparkie

Just my View not to be taken as absolute fact merely a pointer in the right direction.

One other thing before anyone commences proceedings make a CPR 31.16 application for them to supply a copy of the underwritng sheet appertaining to your laon and stress the importnce of the supply of this will have on your ability to pursue your claim......and point out that if this document is not supplied it will substantially weaken your claim and chances of success of your claimLast edited by Sparkie1723; 25th June 2011, 22:53:PM.Leave a comment:

-

Re: Swift Advances Plc?

A little advice!

If you have cause to speak to Swift Group Legal Services on the phone for any reason and you have the BT service that gives you free calls to any BT landline do not call on the 0845 number as this is charged at a higher rate than a normal call as you know, this is why they keep you holding for as long as possible, they make money from this number.

Call Swift Group Legal Services on their own direct line 0277359466, this is a further indication that they do class themselves as a separate firm and not a department within Swift Advances plc like the credit control and compliance department, as they try to make you believe

The above number is the one supplied to the Law Society and shown on their registration as the number for the "Organisation" Swift Group Legal Services.

I was not going to post further info, as I heard some people were having doubts about some of my posts.

But as this will save Swift Borrowers money I thought I would over rule myself.

SparkieLeave a comment:

-

Re: Swift Advances Plc?

Compliments of Sparkie

NOTE FOR THE PUBLIC REGISTER UNDER SECTION 35 OF THE

CONSUMER CREDIT ACT 1974 (THE ACT)

LICENCE NO: 391 61 8

LICENSEE: SWIFT ADVANCES PLC

DETERMINATION OF MINDED TO IMPOSE REQUIREMENTS

NOTICE

An adjudicator, acting on behalf of the Office of Fair Trading (OFT), served

a notice on the licensee that she was minded to impose requirements on the

licensee. The adjudicator received representations from the licensee.

SUMMARY OF REASONS FOR ADVERSE DETERMINATION

Having considered the representations, the adjudicator decided to impose

the following requirements:

Underwriting

The Licensee will ensure that its underwriting decisions are subject to a proper assessment of the borrower's ability to meet repayments on the loan in a sustainable manner and without undue hardship and without resort to the security, taking account of relevant circumstances and any reasonably foreseeable future circumstances.

Specifically the Licensee must

a) verify income (s)declared by prospective borrowers;

b) take appropriate account of a potentia! borrower's other financial commitments;

c) take appropriate account of a potential borrower's individual financial and personal

circumstances;

d) give appropriate consideration to all information which is obtained by the licensee in the course of assessing an application;

e)ensure that its underwriting procedures are compliant with the Second Charge Lending Guidance, particularly the General Principle as stated at paragraph 2.1 which states that all underwriting decisions should be subject to aproper assessment of the borrower's ability to repay the loan without undue hardship and without resort to the security. In so doing, the Licensee will take full account of all relevant circumstances and any reasonably foreseeable future circumstances.

Arrears management

The Licensee must use litigation as a last resort and only where a

borrower is unable to meet his commitments in the long term or unwilling to engage with the Licensee; ensure that its communications with customers accurately reflect its authority and the correct legal position, in accordance with paragraphs 2.3 and 2.4d of the OFT'S Debt Collection Guidance July 2003, updated December 2006

Default charges

The Licensee must

a) ensure that the tariff of charges gives a clear explanation of when charges will be applied to an account and what they are for;

The Licensee's charges should be set out clearly and fully as part of the credit agreement and in periodic statements,

Notice of any appeal, which must be given within 28 days of the date on

which notice of the determination is issued, and of its result, will be put on the public register.

PLEASE NOTE THAT THESE PROCEEDINGS ARE NOT THE SAME AS THOSE OF A COURT. THEREFORE A FINDING THAT A PERSON HAS ENGAGED IN CONDUCT WHICH AMOUNTS TO AN OFFENCE OR

CONTRAVENTION OF A STATUTE DOES NOT MEAN THAT THE PERSON CONCERNED HAS BEEN CONVICTED OF THAT OFFENCE OR BEEN FOUND BY A COURT TO HAVE CONTRAVENED THAT STATUTE.

DATE OF DETERMINATION: 17 JUNE 201 1Leave a comment:

-

Re: Swift Advances Plc?

OFT threatens to cancel Swift's licence

23 June 2011 | By Natalie Thomas

Sub-prime lender Swift, trading as Swift Advances and Swift Securities, must improve its lending and collections practices or it risks losing its credit licences.

An Office of Fair Trading investigation found Swift was giving secured loans to customers with poor credit histories or limited access to credit without:- checking whether they could afford the loan

- verifying their income

- taking account of their other financial commitments and personal circumstances

- fully checking the information provided in the application.

As a result, the OFT has imposed a set of requirements on Swift, which ensures it must:- carry out proper assessments of a borrower’s ability to repay the loan without undue hardship

- only take steps to repossess a borrower’s home as a last resort

- be transparent about their charges and when they apply.

David Fisher, director of consumer credit at the OFT, says: “Credit businesses must lend responsibly - failure to do so can have a very serious impact on borrowers. We require Swift to significantly improve the way it carries out its business. If they fail to comply with these requirements, they will face further enforcement action.”

Sparkie

Leave a comment:

-

Re: Swift Advances Plc?

To show further how Mr Webster tries to turn everything upside down ...he forgets what he says.

In August 2009 in an e-amil to me .....He said this....

Quote

There was no legal transfer of the mortgage from Swift Advances to Kestrel Loans no 1- this was an internal accounting procedure only. The morgage has at all times remained in the name of Swift Advances plc.

Then in September 2009 he said this.

In a sincere attempt to save you from unnecessary legal expense, please note:

The transactions referred to in our accounts refer to loans that were sold by equitable assignment which is a valid and enforceable sale that transfers all the benefits, interest and liabilities of the loan, title has always remained with the lender.

Our Loan was transferred to Kestrel Loans No 1 Ltd on 18th April 2007 recorded in our History notes

How does he explain the two accounts then shown previously this internal accounting procedure was as I allege.....double accounting......that's his procedure making it appear both companies are receiving money to make their books look good. To present to the funding Banks to borrow more money.

I will be posting where and how they apprioached two different banks on the same day to borrow the same amount of money using these double accounts.

I have the documents they used.

I will also be posting later on a debenture being signed off as satisfied by Mr Mathew Payne one of their in House solicitors acting as a Commissionaire of Oaths inside Arcadia House.

This was totally unlawful act….. a solicitor who has been and is involved and has any interest what so ever in the company CANNOT act as a Commissionaire and carry out that duty in that capacity. The parties to the signing of this legal document were Mr Sunny Lo company secretary of Swift Advances plc and Mr Mathew Payne.

Mr Payne may try to counter this by saying that he was at the time a solicitor employed by JW Godfrey & CO who was an independant sole Practioner..............but JW Godfrey & CO operated from Swift Advances plc offices at Arcadia House and were acting as their in house solicitors in the direct employ of Swift Advances plc.......and from what I can trace he did not submit accounts of his own to the SRA or to Companies House.

Commissioner for Oaths are most usually Solicitors or qualified Notaries Public but other people within the legal profession such as Barristers, Legal Executives and Licensed Conveyancers are just as qualified to fulfill this role. Be aware, however, that a Solicitor is forbidden to act as a Commissioner of Oaths in any proceedings in which they have a vested interest.

SparkieLeave a comment:

-

Re: Swift Advances Plc?

With ref to our two account docs.

These two separate entirely different companies use these payments as assetts in their company accounts.

That is double accounting and fraud in my opinion.

But what is significant about Kestrel Loans No 1 Ltd is that it holds no CCA licence .......FSA licnece or .....DPA licence....

But as it bought both regulated and unregulated loans ....it also boufght Swift 1st Ltd Mortgages.

THey are breaking every rule ion the Book.................the same Directors are the directors of these two companies.

I hope the clever Barristers that represent SWift Advances plc and Swift 1st Ltd are looking at this thread, and hope they realise that they are assisting both of these companies to repossess house under false double accounting procedures.

Mind you these Barristers are not human beings are they?...........just greedy!!

I have three or four other customers records to back mine up....these customers did not realise how important and serious this was and how it affects their cases,

I also hope that somewhere a police officer will be reading this thread.......I have the evidence ....and lots of it.

Its time now for these directors to be called in to answer some searching questions in my opinion, before they ruin more peoples lives by repossessing their homes while all this is going on.

Finally on this No one will convince me that the staff/employees of SWift Advances plc do not know what is going on....they are the ones that operate these computer systems .....they are just as responsible as anyone and should pay the price when the time comes....if I were them I'd get off the boat before it sinks....just my opinion

SparkieLeave a comment:

-

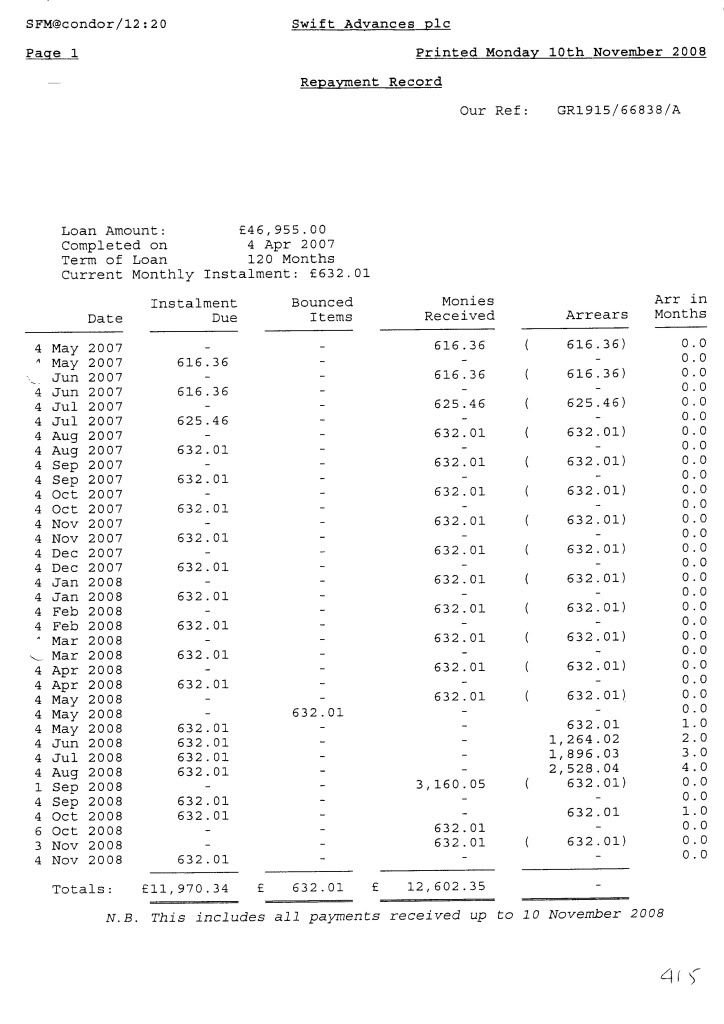

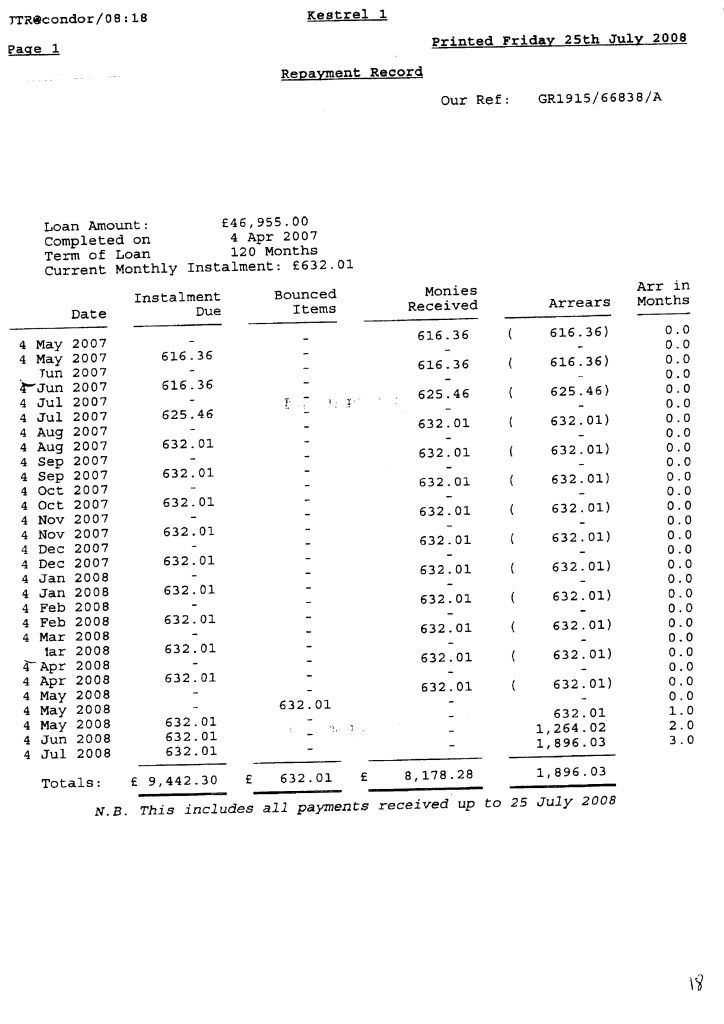

Re: Swift Advances Plc?

Here is the proof of the double accounting ...I'll say a bit more about in a minute

Sparkie

Note they both say they receive these payments at the bottom............also our loan started on 4th April 2007 as shown on these two records with the two companies....yet we only signed an agreement with Swift Advances plc.Last edited by Sparkie1723; 20th June 2011, 15:31:PM.Leave a comment:

-

Re: Swift Advances Plc?

Will post the two docs here when I have edited them.....didn't work the first time

SparkieLast edited by Sparkie1723; 20th June 2011, 12:41:PM.Leave a comment:

-

Re: Swift Advances Plc?

Sorry folks double post

SparkieLast edited by Sparkie1723; 20th June 2011, 13:25:PM.Leave a comment:

Leave a comment: