Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

A brief update on my VT - they are claiming I need to pay Ł183 for collection of the vehicle as per my t&c's.

I don't have the paperwork to hand, but going by other posts I'm guessing they are at it?

Edit: checked & section 10 they are quoting refers to early termination BY THEM. Total chancers!

One strongly worded reply coming up!

Loading...

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Hi,

I've sent my letter of VT to FCA today. My next payment is due on 2nd October, will I still have to make this payment or can I cancel my direct debit?

Thanks,

AshleyLeave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

I'd just like to post my thanks at this time to everyone putting so much hard work into this thread.

Using the in depth template from page 1, I am now mid VT with Startline.

As expected after reading on here, they've sent me a VT form and I've just replied advising I will not be signing as the agreement has already been terminated as per my initial letter. I also added a line advising ther is no MOT cert due to the car being only 2 & 1/2 years old.

I've requested they get back to me with a mutually agreeable collection date/time, I'll keep y'all updated on the progress.

The KA is in tip top condition, both services performed by Ford, and has had 1 new tyre. Also it has less than 6k miles on the clock.

Will be a nice feeling saving so much money every month now the KA is being handed back!

Cheers,

BLeave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

You can cancel, they have acknowledged receipt and you owe nothing more since it is now terminated.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

I have just filled in the form to exercise my right to an early termination with Peugeot Finance. They have confirmed I have payed over 50% and advised they would be in contact to arrange collecting of my vehicle within 3 weeks.

My question is, The next payment is due out 1st Oct which will be around the date of vehicle collection would I still need to make this payment or could I cancel the direct debit.

Thanks in Advance

KellyLeave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Yes, that is correct. It's 50% of the total amount payable, so deposit+payments+final payment+interest.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Originally posted by Mr.Peterbard View Post

HI Peter,

Your information is very useful.

I am currently trying to VT my Mercedes, I am over the half way point of my 36 month contract but they are saying I have to take in to consideration the final balloon payment at the end of the 3 years? Is this correct?

Thanks,

AlexLeave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

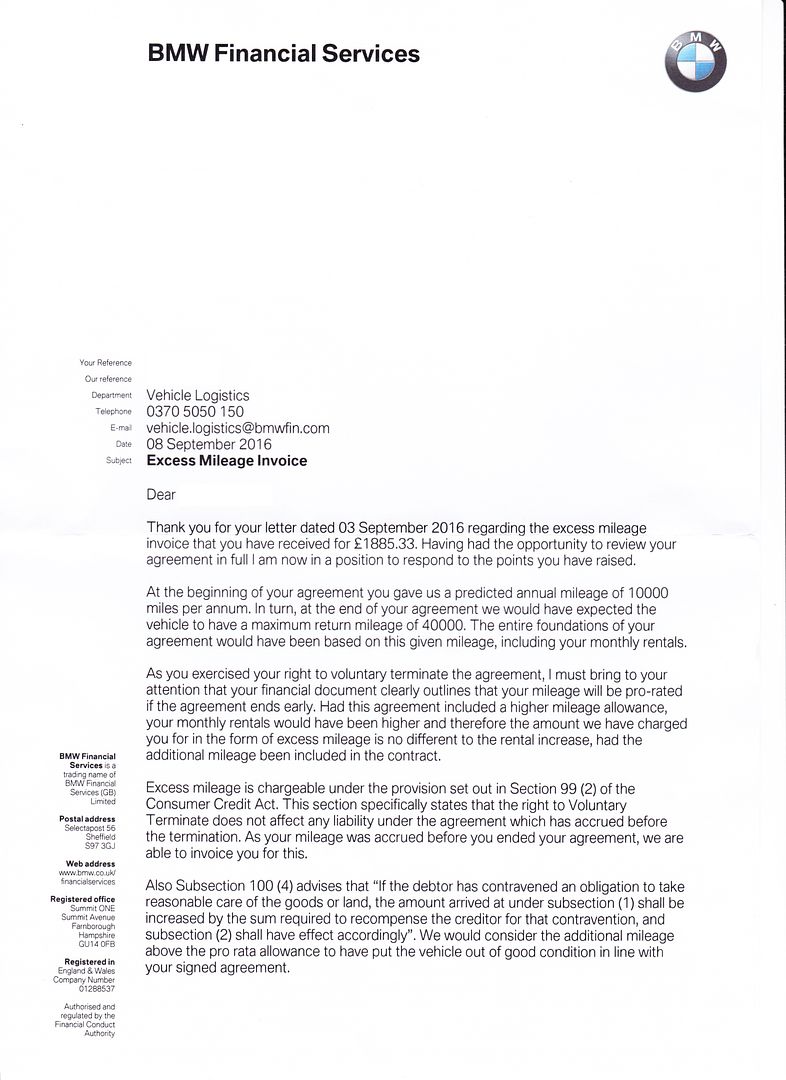

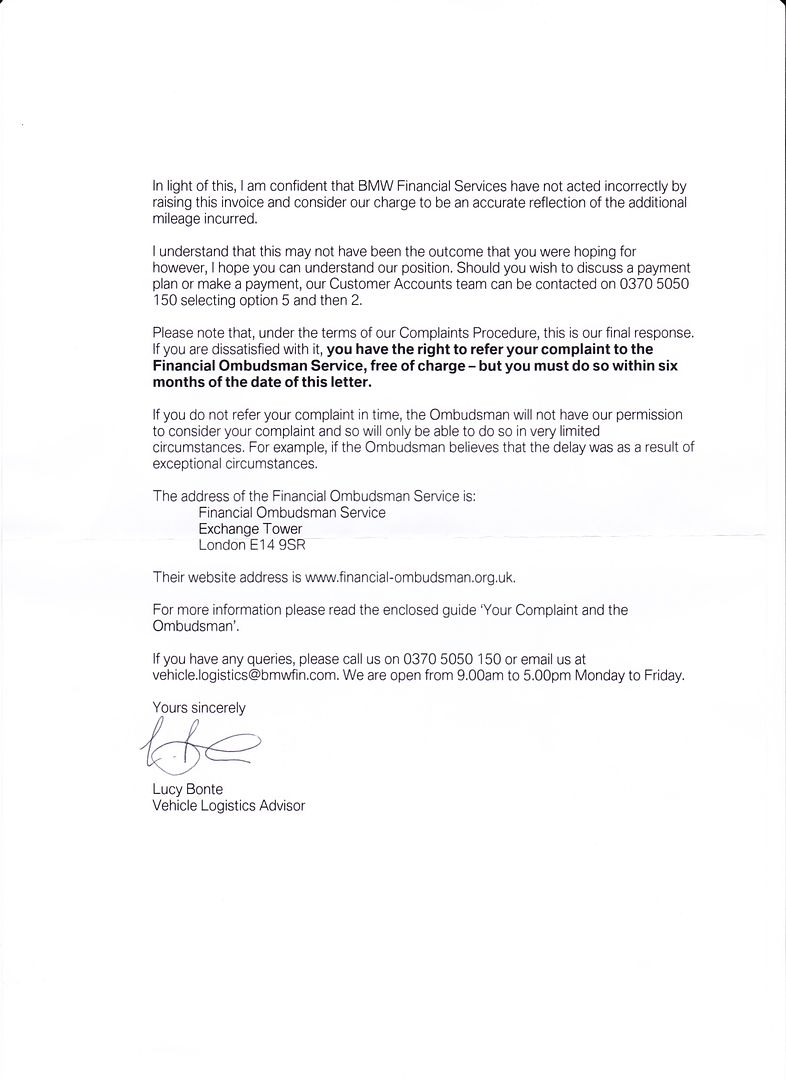

OK.

So I got a response from BMWFS today. I have scanned the letter, blanked the sensitive info, and posted here.

So how do I proceed from here? Should I re-send the excess mileage letter (below), but keeping the reasonable condition part in play? Or go straight to the ombudsman?

Would there be any advantage in starting my own thread, and keeping everything pertinent to my case there? I would be happy to update here too, but it might be "cleaner" if there aren't 40-odd pages around my info. (EDIT: I have started thread here: http://legalbeagles.info/forums/show...ocess-(Aug-16))

Response to lender disputing excess mileage charges

Dear Sir/Madam,

Re: Voluntary Termination

Agreement Number:

Vehicle Registration:

I am writing further to your letter dated [DATE].

Please note that liability in relation to the alleged outstanding balance for excess mileage is denied.

You have suggested in your letter that I am liable to pay excess mileage under the terms of the agreement, however this is not correct. Section 100(1) confirms that liability is restricted to one half of the total price payable. The CCA defines ‘total price’ as “total sum payable by the debtor under a hire-purchase agreement or a conditional sale agreement, including any sum payable on the exercise of an option to purchase, but excluding any sum payable as a penalty or as compensation or damages for a breach of the agreement” (emphasis added).

As you have already alluded to, the excess mileage is a contractual term of the agreement and therefore cannot be included as an amount which is owed. This position is further clarified under section 173 of the Act in that any contractual term which is inconsistent with any rights under the CCA and imposes additional liability, whether direct or indirect, shall be void and unenforceable.

[I note that your letter refers to s.100 of the Consumer Credit Act insofar as the vehicle is not in a reasonable condition as a result of the excess mileage. Despite this claim, you have not provided any evidence outlining specifically the damage caused to the vehicle due to the excess mileage. I am of the opinion that the vehicle was maintained in a reasonable condition throughout the period of the agreement. Therefore, such damage charges you are claiming would amount to fair wear and tear and the vehicle does not need to be returned to you in any better condition other than a reasonable one.]

Nonetheless, the excess mileage clause is based on the principle of ascertaining an estimated value of the car, taking into account its age and anticipated mileage at the end of the hire period. The hirer is then offered the option to purchase the vehicle at the suggested price. Mileage which exceeds the stipulated amount under the terms does not however, mean that the vehicle is not in a reasonable condition.

In any event, such sums you are alleging to be owed may only be recovered by a court order only and should you wish to pursue this matter in court, your application will be strongly defended.

Please confirm by return that this matter is now closed.

Yours faithfully,

[NAME]

Last edited by xs2man; 10th September 2016, 10:47:AM.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Yes it will be the best way, I think the person you are referring to may have bottled it after receiving the letter from BMW's external solicitors and may have put him off but we may or may not find out about that.

Keep us updated on the progress.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

I have no intention of taking out any finance in the short term, so I wont be pressured into handing money over and fighting to get it back (as I noticed someone else on here doing). So I am not too overly worried on that front. Although I would prefer it not to drag on for a year admittedly, as there are some things coming up then.

Anyway, letter was sent recorded delivery, just as I put it. I didn't bother mentioning the actual amount of excess mileage, as I don't intend to pay it. Certainly not at this stage anyway. So thought there was little point in mentioning it just now, and rather wait until it comes to the crunch before going down that route.

Now the wait for the response. I'm sure they will try and call me, but I will simply state I am too busy to speak, and all correspondence should be via letter or email, so that I can review it when I get a chance.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Hello,

The letter is fine by me. As for your excess mileage argument, it is something worth mentioning. however, they could argue that the mileage is calculated until the date of termination, the additional payments to make up the 50% doesn't have anything to do with the calcluation because they have a right by law to a minimum of 50% of the contract, and you can't calculate something based in the future if you are't in possession of it.

That would be my take on their counter argument.

Anyhow, they can't charge for excess mileage but keep an eye on your credit report, Ive heard they threaten to put a default on too.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

OK. So my car was picked up on Tuesday there. Everything went well. Car was one of the best condition motors the boy had seen. He did pick up some dodgy wheel repairs (virtually unnoticeable), but since it was BMW who done them, they can jump for that, lol.

Anyway, so they sent me out an invoice for excess mileage, as expected. Now obviously I am going to fight it, and will be sending this letter:

I haven't put in the agreement number or anything here, but are in the letter to be sent.I am writing further to your letter dated 01/09/2016.

Please note that liability in relation to the alleged outstanding balance for excess mileage is denied.

You have suggested in your letter that I am liable to pay excess mileage under the terms of the agreement, however this is not correct. Section 100(1) confirms that liability is restricted to one half of the total price payable. The CCA defines ‘total price’ as “total sum payable by the debtor under a hire-purchase agreement or a conditional sale agreement, including any sum payable on the exercise of an option to purchase, but excluding any sum payable as a penalty or as compensation or damages for a breach of the agreement” (emphasis added).

As you have already alluded to, the excess mileage is a contractual term of the agreement and therefore cannot be included as an amount which is owed. This position is further clarified under section 173 of the Act in that any contractual term which is inconsistent with any rights under the CCA and imposes additional liability, whether direct or indirect, shall be void and unenforceable.

Nonetheless, the excess mileage clause is based on the principle of ascertaining an estimated value of the car, taking into account its age and anticipated mileage at the end of the hire period. The hirer is then offered the option to purchase the vehicle at the suggested price. Mileage which exceeds the stipulated amount under the terms does not however, mean that the vehicle is not in a reasonable condition.

In any event, such sums you are alleging to be owed may only be recovered by a court order only and should you wish to pursue this matter in court, your application will be strongly defended.

Please confirm by return that this matter is now closed.

However, what is of some concern, if this doesn't work, is how they have calculated the invoice. The pence per mile is, as far as I recall, wrong, but I will double check that. But they have based it on the mileage for the time I have owned the car, rather than have paid for. So I had to pay out almost 4 months worth of payments, up until roughly the end of December. So I have already paid for the mileage usage up until that point (as I see it), but they are claiming otherwise. Anyway, hopefully it doesn't come down to fighting down that route, as with the extra miles, and the extra cost (ppm), the invoice is roughly double what I was expecting.

Is that letter okay to send like that? It is basically a copy / paste of the letter on the FAQ thread, with the s100 bit taken out, as it was not referred to in the invoice. Or should I be leaving that in?Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Started the VT process with Fiat today, used the template on this forum, ive ignored the letter FCA sent me wanting me to sign accepting costs.

Lets see what happens, I shall keep this updated.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

If you want to potentially waive your limited liability under the CCA and potentially cause further headache, then by all means go ahead and sign it. In my opinion I would strongly advise against signing anything as you are not legally obliged to sign anything other than give notice to terminate. The wording you have supplied indicates a representation that what you say is correct, if it is found out to be incorrect you could be liable for misrepresentation.Leave a comment:

-

Re: Voluntary Termination of a Hire purchase or conditional loan under the CCA 1974

Originally posted by R0b View Post

Thanks Rob

Received a letter from Northridge Finance today, it also came with a checklist. The main body of the letter states...

"....a full condition of your vehicle will be carried on your vehicle to the BVRLA fair wear and tear standard. If there is damage outside this standard you will be liable to pay the specified amount with immediate effect or within the next 10 working days. If you choose not to make payment for damages your account may remain live until this damage claim is paid to Northridge Finance, this is defined within the T&C's of your agreeement - "You must keep the goods in good repair and condition""

The checklist is asking if there is mechanical faults, bodywork intact and if the keys & logbook are there. It also states "If it later transpires that any of the above checklist items has been incorrectly advised, I will remain liable for the cost incurred by the finance company in remedying"

It asks me to sign it and return to the finance company, question is do I do that??Leave a comment:

Leave a comment: